High-Friction Savings: The Psychological Armor for Your Capital in 2026

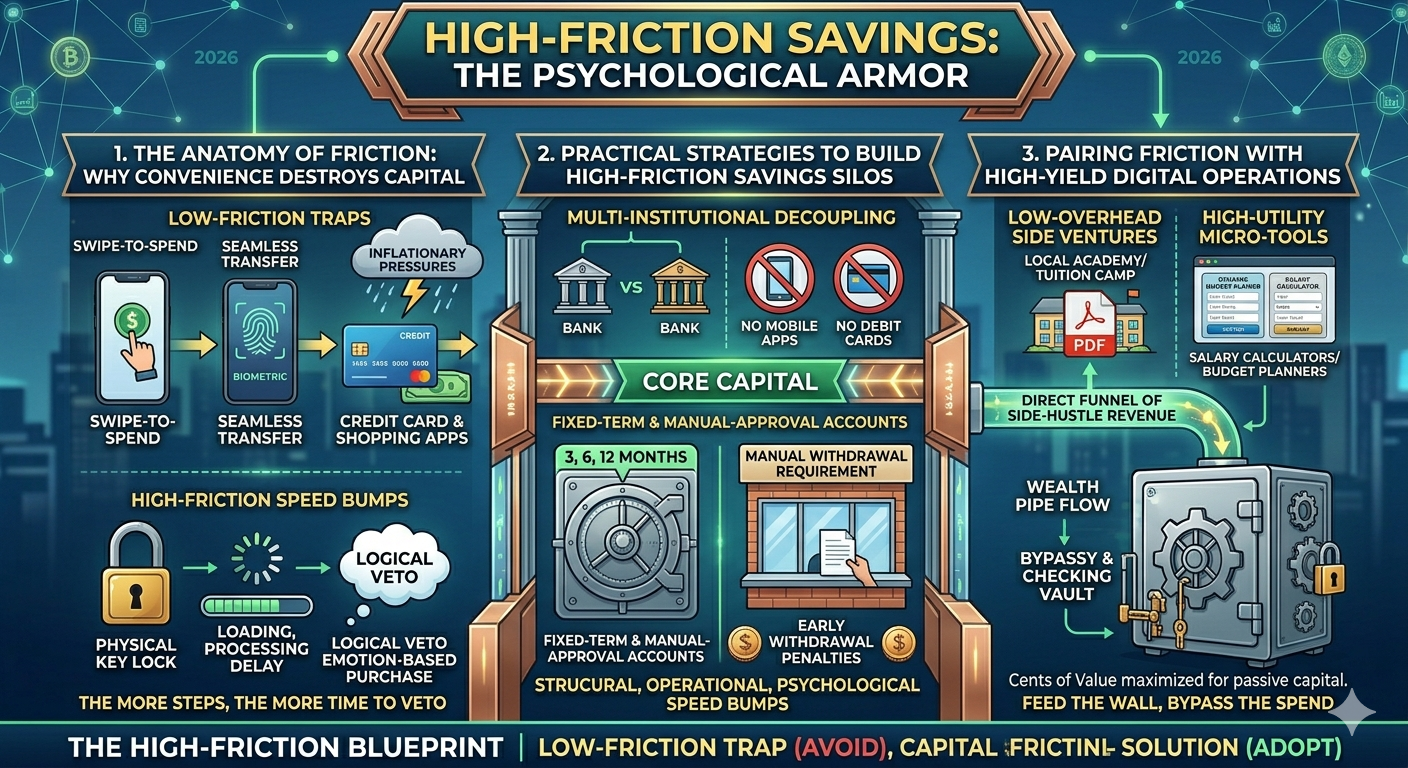

In an economic climate defined by volatile market shifts and persistent inflation, the traditional approach to saving money is no longer sufficient. Most standard banking mobile apps are built for ultimate convenience: with a single swipe, funds move instantly from a savings wallet to a checking account, ready to be spent. While seamless friction is great for user experience, it is disastrous for capital preservation.

To protect your financial status today, you must intentionally slow down your access to your own money. This defensive strategy is known as High-Friction Savings—the practice of utilizing deliberate banking barriers to shield your core capital from impulsive spending and inflationary pressures.

1. The Anatomy of Friction: Why Convenience Destroys Capital

When inflation pushes the baseline cost of everyday goods higher, psychological spending triggers alter. When money feels like it is losing value, the human brain is naturally tempted to spend it quickly on short-term upgrades or non-essential overhead before prices rise further.

Traditional savings accounts offer “low friction,” meaning your money is only a notification or biometric scan away from being liquefied. High-Friction Savings flips this model by reintroducing structural, operational, and psychological speed bumps between you and your cash reserves.

The Friction Rule: The more steps required to execute a withdrawal, the more time your logical brain has to veto an impulsive emotional purchase.

2. Practical Strategies to Build High-Friction Savings Silos

Implementing a high-friction model does not mean hiding cash under a mattress; it means using modern financial structures to build intentional barriers.

Multi-Institutional Decoupling

The simplest way to create friction is to separate your primary income stream from your primary wealth-building repository.

-

No Mobile Apps: Open a savings account with an entirely different financial institution than your everyday transactional bank. Crucially, do not install that bank’s mobile app on your smartphone.

-

Eliminate Debit Cards: Refuse or immediately destroy any ATM or debit cards linked to that specific savings repository.

Fixed-Term and Manual-Approval Accounts

To insulate your capital from rapid-fire online transactions, choose account architectures that strictly enforce processing delays.

-

Time-Locked Deposits: Utilize fixed-term instruments where funds are legally or structurally locked away for 3, 6, or 12 months. Early withdrawal penalties act as a powerful financial deterrent.

-

Manual-Withdrawal Requirements: Choose account types that do not support online bank transfers (IBFT) or digital payment gateways. Forcing yourself to physically visit a brick-and-mortar branch or submit a manual paper request to access funds ensures that only true emergencies will prompt a withdrawal.

3. Pairing Friction with High-Yield Digital Operations

While building your defensive high-friction wall, your offensive strategy must focus on continuously feeding that wall with new revenue. For digital entrepreneurs, educators, and bloggers, the cash generated from low-overhead ventures should feed directly into these high-friction repositories, completely bypassing checking accounts.

┌───────────────────────────────┐

│ Low-Overhead Side Ventures │

│ (Local Programs / Blogs / etc)│

└───────────────┬───────────────┘

│

▼ Direct Transfer

┌───────────────────────────────┐

│ HIGH-FRICTION SAVINGS │

│ (Time-Locked / No Mobile App)│

└───────────────┬───────────────┘

│

[Intentional Barriers]

│

▼ Delayed Access

┌───────────────────────────────┐

│ Essential Overhead │

│ (Audited Monthly Budget) │

└───────────────────────────────┘

Automating the Wealth Pipe:

-

Monetize with High-Utility Widgets: If you manage a web platform, boost your incoming ad revenue by embedding lightweight, custom HTML/CSS micro-tools—such as interactive calculators or data formatters—into your theme layout. The massive user dwell time maximizes your AdSense RPM (Revenue Per Mille), creating a steady stream of passive capital.

-

Funnel Local Income Streams: If you run real-world community projects (like a seasonal tuition camp or training academy), leverage zero-cost digital infrastructure. Route parents to online downloadable PDF registration sheets, and ensure your promotional flyers display your contact number boldly right at the top for direct inquiries. Take the high-margin revenue from these local operations and immediately deposit it straight into your high-friction accounts.

Summary: The High-Friction Blueprint

| Financial Objective | Low-Friction Trap (Avoid) | High-Friction Solution (Adopt) |

| Emergency Fund Access | Linked savings account with instant mobile transfer. | Secondary bank account with no mobile app installed. |

| Capital Preservation | Flexible savings vaults attached to shopping apps. | Fixed-term deposits with strict early-withdrawal penalties. |

| Cash Flow Control | Disorganized spending directly from incoming revenue. | Direct routing of side-hustle profits into manual-approval accounts. |

By strictly auditing your household overhead and locking your surplus earnings inside high-friction barriers, you neutralize the urge to spend impulsively. In an inflationary economy, real financial security isn’t about how fast you can access your money—it’s about how effectively you can protect it from yourself.